{kind=link}

You may know about the importance of building and maintaining a good personal credit score, but do you know that businesses also need to have good credit? If you are a business owner, learn all about business credit scores in this blog.

Business credit scores are not that different from personal credit scores, but there are some key differences in how they are put together. This is where you can learn how a business credit score is constructed, the importance of a high score, and what you need to do to ensure your business has a strong credit profile.

What is a business credit score?

When you need to take out a business loan or open a line of credit, the lender or service provider will typically check your personal and business credit history to determine your eligibility. All types of businesses have business credit scores. The only requisite is to have suppliers, vendors, and lenders who regularly report account activity to a credit bureau.

Why is a business credit score important?

It becomes easier to get financing when you have a good business credit score. If you don’t, you’ll have to rely on personal savings, credit cards, home equity, and other ways of financing.

With a good business credit score, the lender will not require a personal guarantee from you. This means they won’t go after your personal assets in case you miss your payment or default.

How do business credit scores work?

Dun & Bradstreet (D&B), Equifax, Experian, and FICO are the four major credit bureaus that generate business credit scores. They use information, such as when your business commenced its operations, credit lines, and payment history to calculate the credit score of your business.

Typically, the most common credit scores range from 0 to 100 except for FICO, which is from 0 to 300. A score in the top 20% of the range is considered good. Make sure to pay all your business obligations on time or early to maintain a strong credit score.

How are they calculated?

Credit bureaus that produce business credit scores are more secretive, while basic calculation for personal credit scores, like FICO, is public knowledge. All the agencies have their own formula, and most of them don’t disclose their scoring algorithm to anyone.

It is up to business credit reporting agencies to consider company information, industry, credit utilization ratios, payment history, and overall financial performance while calculating a business credit score. Experian, Equifax, and D&B additionally collect payment data reported by lenders and vendors.

How are they used?

Like personal credit scores, business credit scores, representing a company’s financial performance, are used to qualify businesses for financing. Lenders, vendors, and creditors use a company’s credit score to determine its creditworthiness. Similarly, a prospective client may look at your credit score to determine the probability of getting paid on time.

The most common types of business credit scores.

The most common types of business credit scores business owners should be aware of are:

- D&B PAYDEX Score

- Experian Intelliscore

- The FICO Small Business Scoring Service Credit Score

- Equifax Business Credit Risk and Business Failure Score

Here’s how each one works.

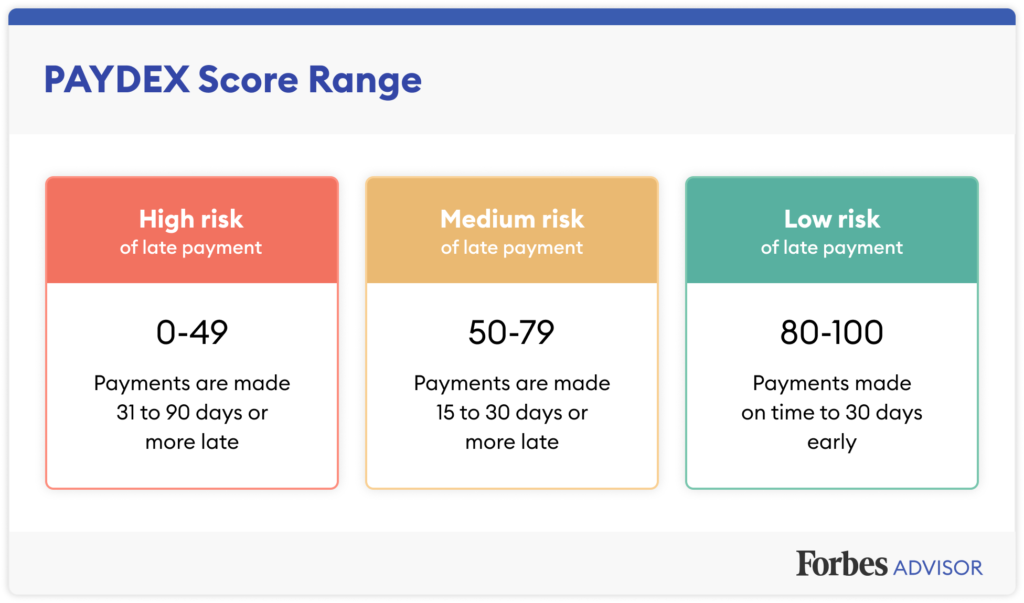

Dun & Bradstreet PAYDEX Score

A score of 80 is considered good under D&B, which typically ranges from 0 to 100. Early or on-time payments can positively affect your score, whereas late payments can negatively affect your score.

Payments that are late by 30-90 days will have a greater impact on your score than payments late by 15-30 days. Below is the PAYDEX score range for a better understanding.

You’ll need to sign up for a D-U-N-S number on its official website and allow suppliers and vendors to report your payment history to get a D&B PAYDEX Score. You can’t build a PAYDEX credit score if the suppliers and vendors fail to report your activity.

Experian Intelliscore

There are two distinct versions of Intelliscore, which are Intelliscore Plus and Intelliscore Plus v2.

Intelliscore Plus may include your personal credit information if your business is new. While Intelliscore Plus v2 allows you to expedite your credit decisions with access to Experian’s wide range of trade, public records, collection, and firmographic data.

Both models, ranging from 1-100, have the same risk classifications.

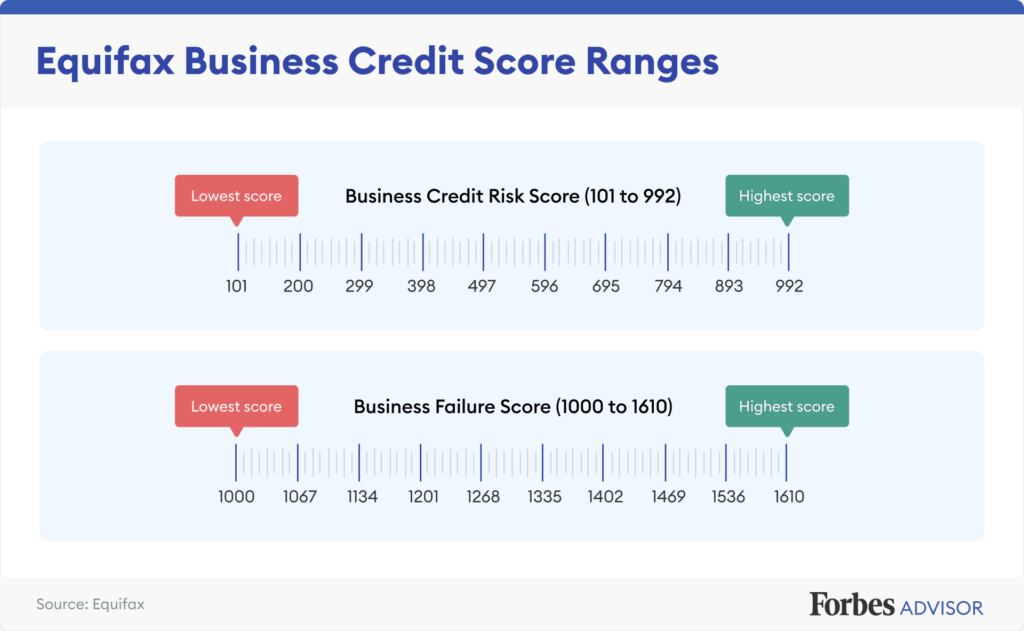

Equifax Business Credit Scores

Equifax generates two business credit scores, which are Business Credit Risk Score and Business Failure Score.

The first one evaluates the probability of a business incurring 90-day severe delinquency or charge-off over the following 12 months. The second one speculates the possibility of a business failing through formal or informal bankruptcy over the next 12 months.

Both scores reflect bankruptcies, liens, on-time payment history, and more. They’ll also show your payment trend for the last 12 months and compare that to the industry average.

The Business Credit Risk Score ranges from 101-992 and the Business Failure Score ranges from 1,000-1,610.

FICO SBSS Credit Score

FICO is not one of the main business credit reporting bureaus, however, it generates one of the most common business credit scores, the FICO Small Business Scoring Service Credit Score. Lenders use this score while qualifying applicants for Small Business Administration Loans.

The FICO score ranges from 0-300, but you’ll need a minimum score of 155 to qualify for the SBA’s pre-screen process. Though, most lenders require a minimum score between 160 and 165.

Furthermore, FICO uses both personal and business information to compile the score. FICO includes personal credit information for the business owners with a 20% stake or more, up to five individuals in total. FICO also considers other business information, such as total revenue, number of employees, time in business, debts, and more.

Final thoughts

Business credit scores aren’t typically free like personal credit scores. To get your business credit score, you’ll need to purchase it from either of the business credit bureaus listed above. You can also use a subscription-based business credit scoring website to retrieve your business credit scores.

By keeping a regular check on your business credit score, you can identify potential threats early on. It is all the more important to be watchful than ever now because business identity theft rose about 258% in 2020, according to D&B’s data.

If you have bad credit and are looking to boost your credit score, credit repair or credit restoration services like CoolCredit can simplify the process for you. Visit www.coolcredit.com to get a better understanding of your credit score.